Consolidation and you, revisited

[Editor’s note: The more things change, the more they stay the same. Or do they? With the mergers of BMC and Stock, Builders FirstSource and ProBuild and a steady stream of acquisitions in the news, it certainly seems like consolidation is raging. We turned to Paul Hylbert, of Kodiak Building Partners for a deeper analysis.>

M+A activity continues to make the news in our building products distribution business, so Ken Clark asked me to take a look back at an article I had written 14 years ago for his publication, then called Home Channel News.

The author tackled the consolidation topic in the Jan. 24, 2005 issue of Home Channel News, the forerunner of HBSDealer.

The author tackled the consolidation topic in the Jan. 24, 2005 issue of Home Channel News, the forerunner of HBSDealer.

So, has anything changed? Are there major differences in the business climate today than in the one we remember way back when?

Other than the dramatic changes in technology which impacts the way we do business, the climate around consolidation is remarkably similar.

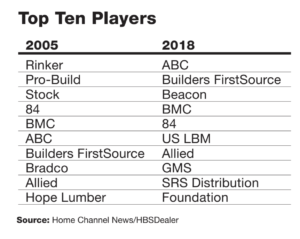

There continue to be many larger firms acquiring smaller ones. Some of the names are the same, and many are different.

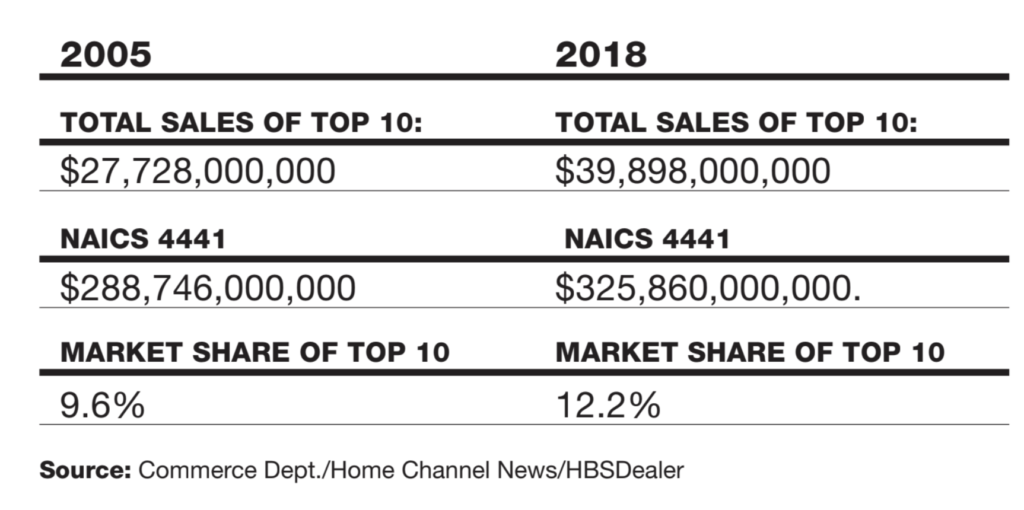

The biggest of the big are larger now, with ABC hitting $10 billion-plus in sales in 2018. (ProBuild in 2006 hit $6 billion.) But the market share of the top 10 firms, is just a bit higher now at 12% than it was 13 years ago at roughly 10%. Independents of all shapes and sizes continue to be the predominant players in this fragmented segment of industry.

There’s also more diversity now among the larger players. The specialty roofing guys have gone into gypsum, the gypsum guys have gone into insulation, and some LBM distributors are into just about all product lines (except plumbing, HVAC and electrical).

What’s happened to our customer base? After shrinking significantly during our housing downturn, the biggest of the big builders are again pushing 40,000 to 50,000 starts, right where they were back in 2008. The difference today is that instead of building 1.8 million to 2.0 million homes per year, we’re only building 1.3 million. That disparity creates a situation where the larger builders have gained share, but almost entirely in the top 100 markets.

So, consolidation continues to be a factor on both the customer and distributor segments of our business, even though our industry remains highly fragmented.

So, consolidation continues to be a factor on both the customer and distributor segments of our business, even though our industry remains highly fragmented.

What does that mean for us as dealer/distributors?

Depending upon your position in your market, maybe not a whole lot. If you’re operating in rural markets, serving smaller homebuilders, or focusing on the repair and remodeling market, then consolidation may not have much of an impact. Even then, as the big specialty distributors continue their expansion into ever smaller markets, you will probably have the likes of an ABC, SRS, GMS, Beacon or Foundation acquire or open near you — if they haven’t already.

And then there’s always Amazon. It’s already a large player in hardware, tools and many other products we sell. If they can solve home delivery of groceries, can they solve jobsite delivery of building products? Or would they rather not invest in this dirty, dusty, cyclical, low margin business of ours?

The good news for all of us is that ours is a business where effectiveness at the local level is most critical to success. Building codes, product tastes and requirements, and construction practices vary significantly by market, and that makes the strength of the operating team at the local level the big driver of success. What works in Laredo won’t always work in Roxbury. But strong people with the authority to tailor the assortment of products and services must be present for success.

Drivers of consolidation will remain, and not just because the big want to keep getting bigger.

Many of us, starting with yours truly, are not getting any younger. In fact, our industry has done a poor job in general of preparing our people to take over our businesses. So now, perhaps in the late innings of the current housing cycle and with no family members ready to take over our company, an owner looks for an exit strategy.

On the other hand, the larger firms, many of which are publicly traded or privately funded, need to grow shareholder value. And one way to do that is to acquire another dealer or distributor. Big isn’t necessarily better, but the desire to grow earnings and cash flow propels these companies toward acquisition of competitors.

These forces are at work on the local level, too, as smaller companies are quietly making their own acquisitions.

Against this background, a long-time M+A professional well into his fifth decade in the business commented recently: “I’ve never been busier. At my age I should be slowing down, but the market won’t let me.”

The bottom line is that consolidation is not necessarily good or bad. What’s important is to recognize it’s happening (and will continue) and then decide how to best address it.

Paul Hylbert

Paul Hylbert

# # #

In 2005, Paul Hylbert was CEO of Lanoga Corp. Today, Hylbert is the chairman of Kodiak Building Partners, which he helped create in 2011. Kodiak manages a diverse portfolio of building material companies in 71 locations around the country. For more information, visit www.kodiakbp.com.

M+A activity continues to make the news in our building products distribution business, so Ken Clark asked me to take a look back at an article I had written 14 years ago for his publication, then called Home Channel News.

The author tackled the consolidation topic in the Jan. 24, 2005 issue of Home Channel News, the forerunner of HBSDealer.So, has anything changed? Are there major differences in the business climate today than in the one we remember way back when?

Other than the dramatic changes in technology which impacts the way we do business, the climate around consolidation is remarkably similar.

There continue to be many larger firms acquiring smaller ones. Some of the names are the same, and many are different.

The biggest of the big are larger now, with ABC hitting $10 billion-plus in sales in 2018. (ProBuild in 2006 hit $6 billion.) But the market share of the top 10 firms, is just a bit higher now at 12% than it was 13 years ago at roughly 10%. Independents of all shapes and sizes continue to be the predominant players in this fragmented segment of industry.

There’s also more diversity now among the larger players. The specialty roofing guys have gone into gypsum, the gypsum guys have gone into insulation, and some LBM distributors are into just about all product lines (except plumbing, HVAC and electrical).

What’s happened to our customer base? After shrinking significantly during our housing downturn, the biggest of the big builders are again pushing 40,000 to 50,000 starts, right where they were back in 2008. The difference today is that instead of building 1.8 million to 2.0 million homes per year, we’re only building 1.3 million. That disparity creates a situation where the larger builders have gained share, but almost entirely in the top 100 markets.

So, consolidation continues to be a factor on both the customer and distributor segments of our business, even though our industry remains highly fragmented.What does that mean for us as dealer/distributors?

Depending upon your position in your market, maybe not a whole lot. If you’re operating in rural markets, serving smaller homebuilders, or focusing on the repair and remodeling market, then consolidation may not have much of an impact. Even then, as the big specialty distributors continue their expansion into ever smaller markets, you will probably have the likes of an ABC, SRS, GMS, Beacon or Foundation acquire or open near you — if they haven’t already.

And then there’s always Amazon. It’s already a large player in hardware, tools and many other products we sell. If they can solve home delivery of groceries, can they solve jobsite delivery of building products? Or would they rather not invest in this dirty, dusty, cyclical, low margin business of ours?

The good news for all of us is that ours is a business where effectiveness at the local level is most critical to success. Building codes, product tastes and requirements, and construction practices vary significantly by market, and that makes the strength of the operating team at the local level the big driver of success. What works in Laredo won’t always work in Roxbury. But strong people with the authority to tailor the assortment of products and services must be present for success.

Drivers of consolidation will remain, and not just because the big want to keep getting bigger.

Many of us, starting with yours truly, are not getting any younger. In fact, our industry has done a poor job in general of preparing our people to take over our businesses. So now, perhaps in the late innings of the current housing cycle and with no family members ready to take over our company, an owner looks for an exit strategy.

On the other hand, the larger firms, many of which are publicly traded or privately funded, need to grow shareholder value. And one way to do that is to acquire another dealer or distributor. Big isn’t necessarily better, but the desire to grow earnings and cash flow propels these companies toward acquisition of competitors.

These forces are at work on the local level, too, as smaller companies are quietly making their own acquisitions.

Against this background, a long-time M+A professional well into his fifth decade in the business commented recently: “I’ve never been busier. At my age I should be slowing down, but the market won’t let me.”

The bottom line is that consolidation is not necessarily good or bad. What’s important is to recognize it’s happening (and will continue) and then decide how to best address it.

Paul Hylbert# # #

In 2005, Paul Hylbert was CEO of Lanoga Corp. Today, Hylbert is the chairman of Kodiak Building Partners, which he helped create in 2011. Kodiak manages a diverse portfolio of building material companies in 71 locations around the country. For more information, visit www.kodiakbp.com.